Gaap Depreciable Life Of Solar Panels

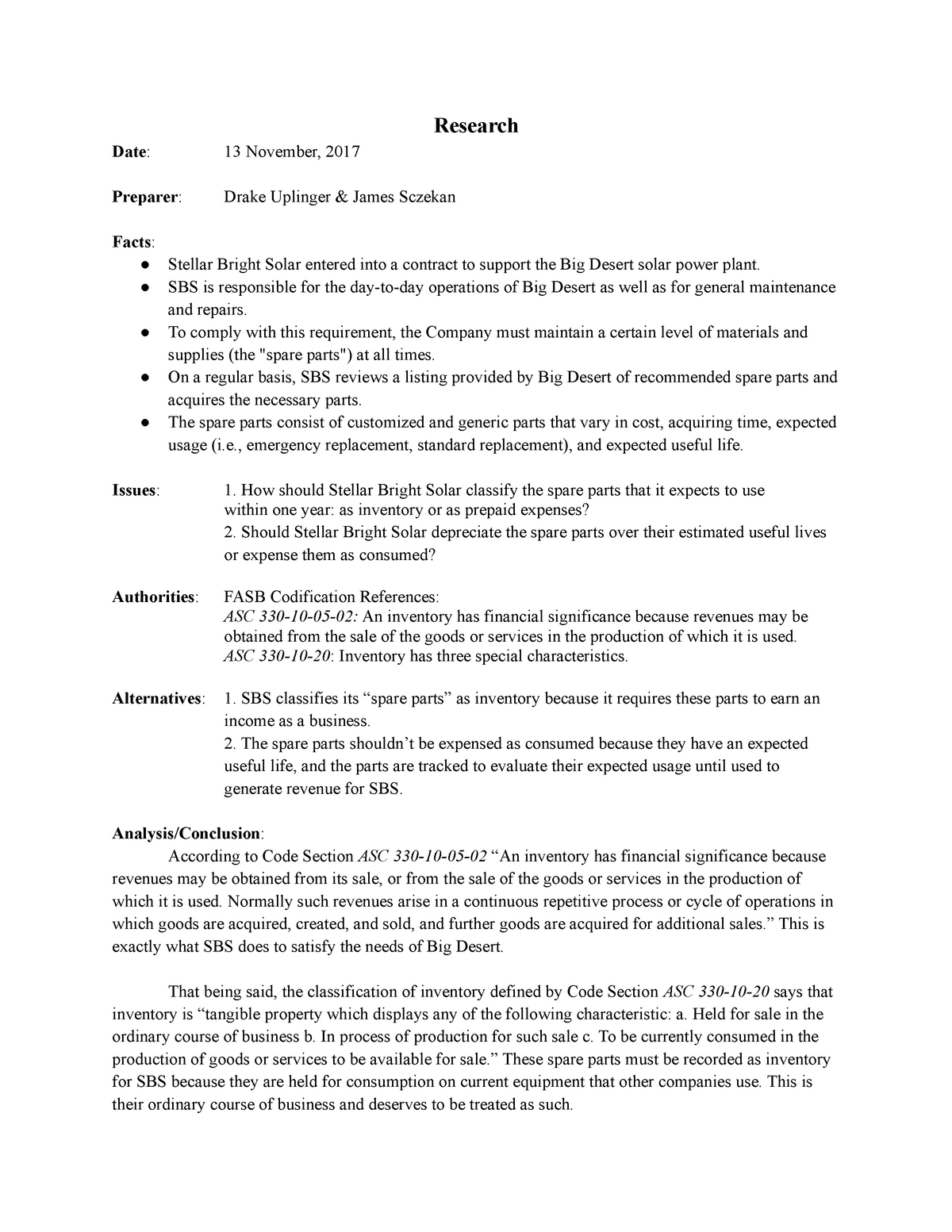

Solved Stellar Bright Solar Sbs Or The Company Is A B Chegg Com

Accounting For Renewable Energy Investments Pdf Free Download

Tax Equity 201 Partnership Flips In Detail Woodlawn Associates

20 2 Financial Reporting Considerations Related To Covid 19 And An Economic Downturn March 25 2020 Last Updated July 8 2020 Dart Deloitte Accounting Research Tool

Economic Margin Applied Finance Capital Management

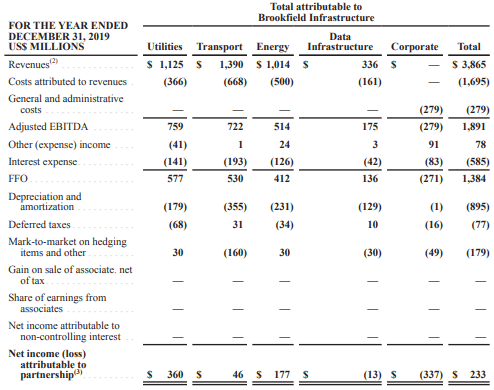

Brookfield Infrastructure Partners Distributions Aren T As Safe As Investors Might Think Nyse Bip Seeking Alpha

Year 1 20 year 2 32 year 3 19 2 year 4 11 5 year 5 11 5 and year 6 5 8.

Gaap depreciable life of solar panels.

Sec Filing Sunpower Corporation

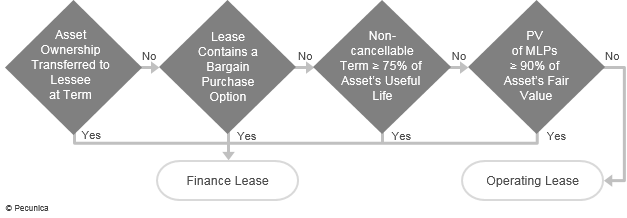

How Do Lessors Classify Leases Under Asc 840 And Ias 17 Pecunica

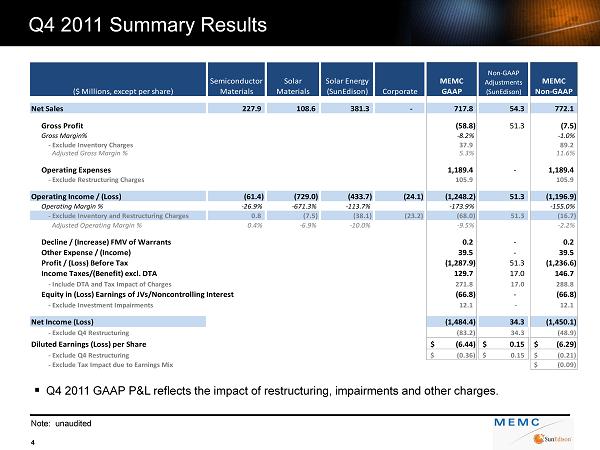

Ex 99 2 3 V302894 Ex99 2 Htm Slide Presentation Memc

An Analysis Of The New Sale And Leaseback Guidance The Cpa Journal

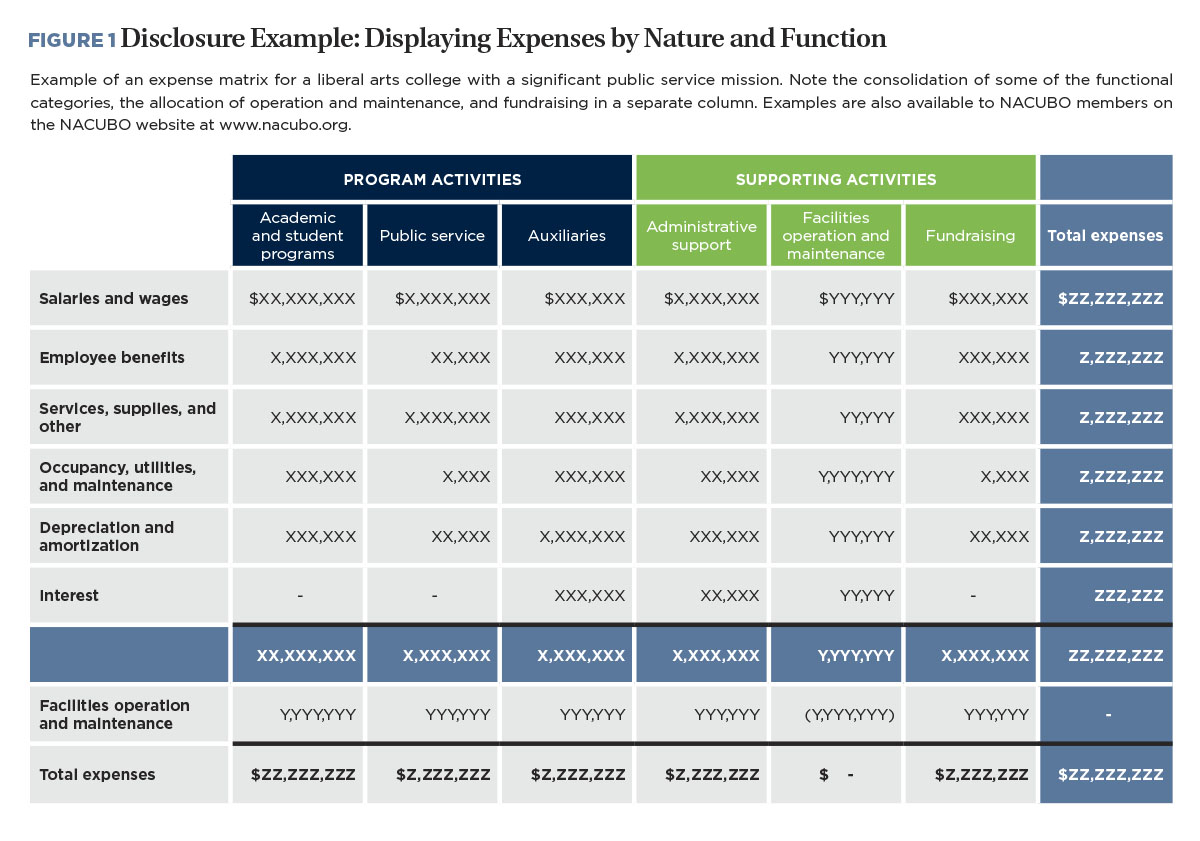

Putting New Rules Into Practice Business Officer Magazine

Ex 99 3

Http Www Investor Nexteraenergy Com Media Files N Nee Ir Investor Materials Supplemental Resources Supplemental Presentations Tax Equity Partnerships Differential Membership Interests Vf Pdf

Acc 301 Research Case Professor Woelfert Acc 301 Cmu Studocu

Investor Presentation

Https Www2 Deloitte Com Content Dam Deloitte Us Documents Energy Resources Us Investments In Renewable Assets By Rate Regulated Utilities Pdf

Sec Filing Mks Instruments Inc

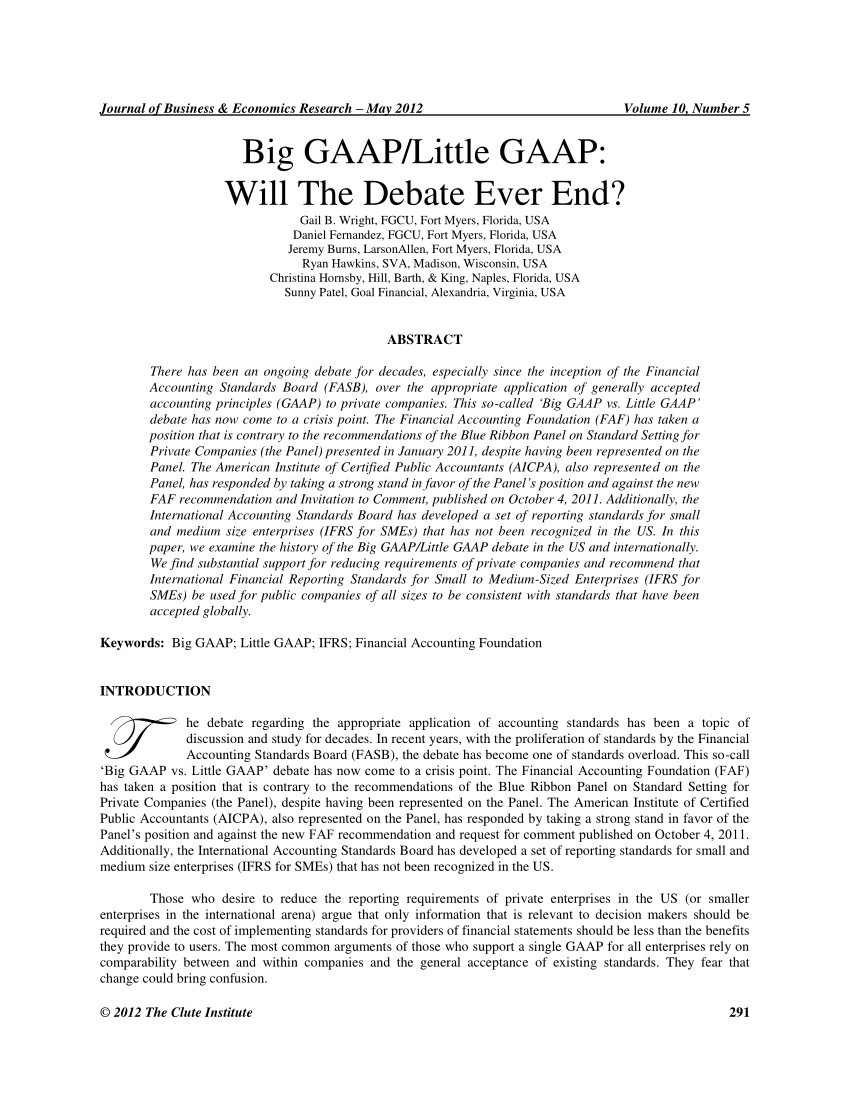

Pdf Big Gaap Little Gaap Will The Debate Never End

Raymondjamespresentation

Commercial Depreciation On A Solar Energy System Yellowlite

99 1

Https Www Mossadams Com Getmedia 77e902ee E8a3 47c5 82e4 Def6c33a6a7a Renewable Energy Tax Credits Pdf Ext Pdf

Form 8 K Northwestern Corp For Sep 10

Ex 99 1

Ic2019

Fcel 8k 20200612 Htm

Ex 99 1

Https Www2 Deloitte Com Content Dam Deloitte Us Documents Energy Resources Us Er Renewable Energy Project Considerations When Transacting With Regulated Utilities Pdf

Https Checkpointlearning Thomsonreuters Com Courses Filedownload Courseidhiddenfield 11666 Deliveryformatidhiddenfield 5

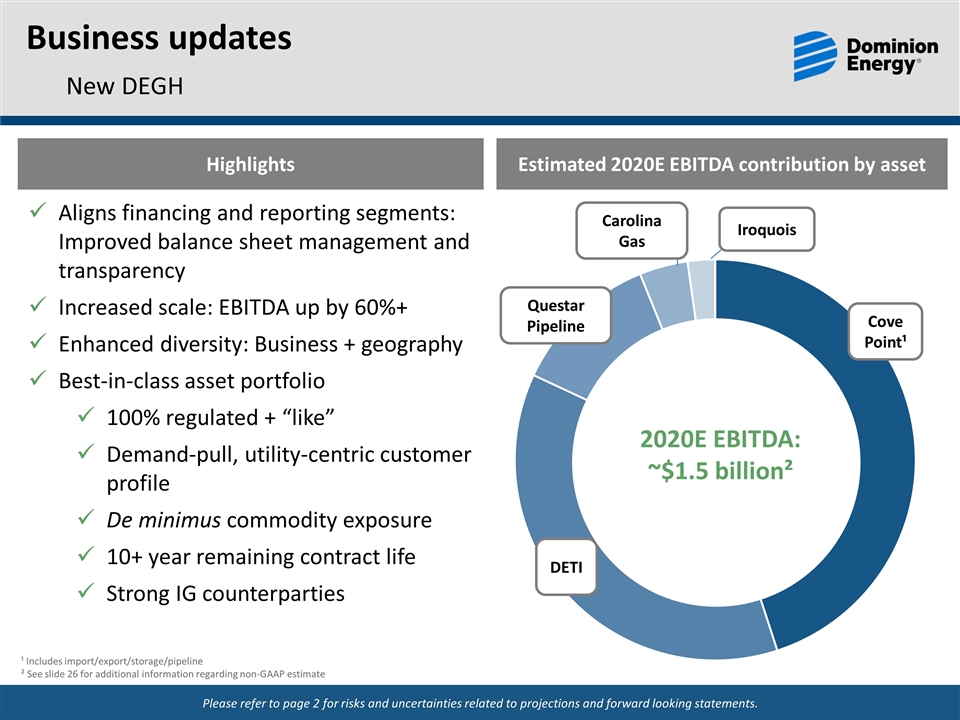

Eixmay2020businessupdate

Source : pinterest.com